Now trading at a price of $71.81, Halozyme Therapeutics has moved 8.1% so far today.

Halozyme Therapeutics returned gains of 32.2% last year, with its stock price reaching a high of $82.22 and a low of $47.5. Over the same period, the stock outperformed the S&P 500 index by 6.3%. More recently, the company's 50-day average price was $65.57. Halozyme Therapeutics, Inc., a biopharmaceutical company, researches, develops, and commercializes of proprietary enzymes and devices in the United States, Switzerland, Belgium, Japan, and internationally. Based in San Diego, CA, the Mid-Cap Health Care company has 423 full time employees. Halozyme Therapeutics has not offered a dividend during the last year.

Increasing Revenues but Narrowing Margins:

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|---|---|

| Revenue (M) | $268 | $443 | $660 | $829 | $1,015 | $1,397 |

| Operating Margins | 54% | 62% | 41% | 41% | 54% | 34% |

| Net Margins | 48% | 91% | 31% | 34% | 44% | 23% |

| Net Income (M) | $129 | $403 | $202 | $282 | $444 | $317 |

| Net Interest Expense (M) | $20 | $8 | $17 | $19 | $11 | $11 |

| Depreciation & Amort. (M) | $3 | $3 | $6 | $11 | $10 | $11 |

| Diluted Shares (M) | 145 | 147 | 141 | 134 | 129 | 124 |

| Earnings Per Share | $0.91 | $2.74 | $1.44 | $2.1 | $3.43 | $2.56 |

| EPS Growth | n/a | 201.1% | -47.45% | 45.83% | 63.33% | -25.36% |

| Avg. Price | $26.41 | $42.22 | $39.76 | $36.96 | $47.74 | $66.41 |

| P/E Ratio | 27.8 | 14.76 | 26.86 | 17.35 | 13.64 | 25.16 |

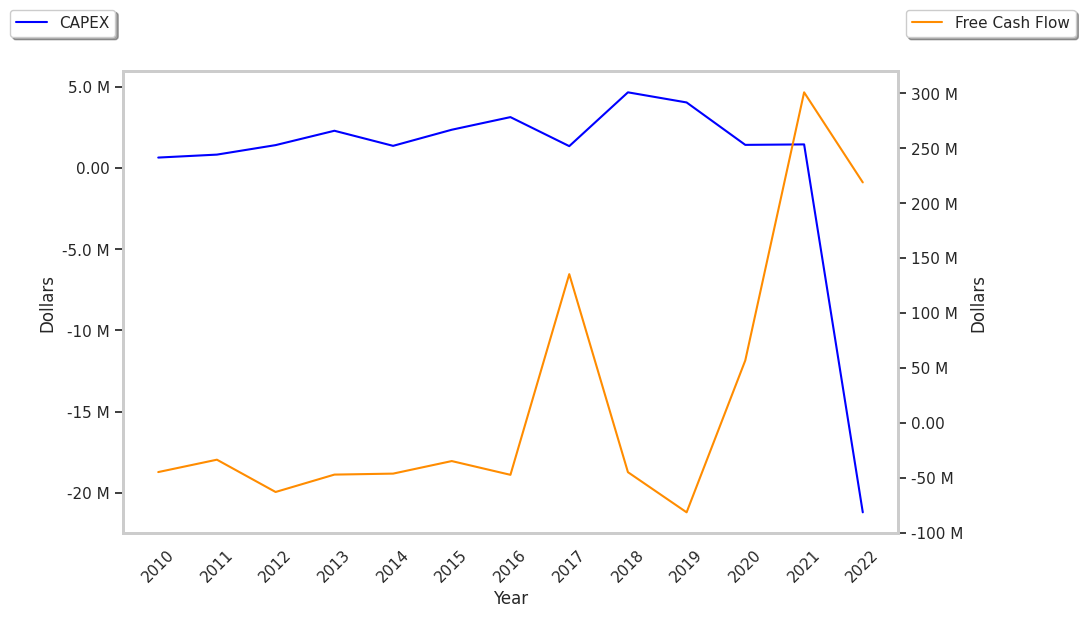

| Free Cash Flow (M) | $53 | $298 | $235 | $373 | $468 | $645 |

| CAPEX (M) | $3 | $1 | $5 | $15 | $11 | $7 |

| EV / EBITDA | 26.43 | 23.2 | 24.67 | 18.31 | 13.25 | 21.21 |

| Total Debt (M) | $397 | $877 | $1,519 | $1,499 | $1,506 | $2,143 |

| Net Debt / EBITDA | 1.69 | 2.72 | 4.69 | 3.96 | 2.47 | 4.18 |

| Current Ratio | 1.32 | 7.91 | 5.65 | 6.64 | 7.8 | 4.66 |

Halozyme Therapeutics has rapidly growing revenues and increasing reinvestment in the business and generally positive cash flows. Additionally, the company's financial statements display an excellent current ratio of 4.66 and a strong EPS growth trend. However, the firm has a highly leveraged balance sheet. Finally, we note that Halozyme Therapeutics has decent operating margins with a negative growth trend.

Halozyme Therapeutics's Valuation Is in Line With Its Sector Averages:

Halozyme Therapeutics has a trailing twelve month P/E ratio of 25.6, compared to an average of 22.94 for the Health Care sector. Based on its EPS guidance of $9.84, the company has a forward P/E ratio of 6.7. According to the 40.5% compound average growth rate of Halozyme Therapeutics's historical and projected earnings per share, the company's PEG ratio is 0.63. Taking the weighted average of the company's EPS CAGR and the broader market's 5-year projected EPS growth rate, we obtain a normalized growth rate of 19.3%. On this basis, the company's PEG ratio is 1.33. This implies that the shares are fairly valued. In contrast, Halozyme Therapeutics is likely overvalued compared to the book value of its equity, since its P/B ratio of 173.47 is higher than the sector average of 3.19. The company's shares are currently trading 1408.7% below their Graham number. Ultimately, Halozyme Therapeutics's strong cash flows, decent earnings multiple, and healthy debt levels factor towards it being fairly valued, its elevated P/B ratio notwithstanding.

Halozyme Therapeutics Has an Average Rating of Buy:

The 9 analysts following Halozyme Therapeutics have set target prices ranging from $57.0 to $96.0 per share, for an average of $85.78 with a buy rating.

Halozyme Therapeutics has an unusually large proportion of its shares sold short because 15.7% of the company's shares are sold short. Institutions own 109.2% of the company's shares, and the insider ownership rate stands at 1.11%, suggesting a small amount of insider investors. The largest shareholder is Blackrock Inc., whose 11% stake in the company is worth $944,644,272.